There have been a lot of discussions recently about the impacts of the recently proposed tariff changes by the US Administration on Chinese goods. As we approach the up-and-coming implementation date of July 6th, 2018, the questions we’re getting from customers about the impact on their products have increased quite a bit. In this post, we’ll break down what types of materials are impacted and the effect it may have on individual products and the market as a whole.

The list of impacted items is weighted away from consumer goods and towards components of consumer goods and ready-to-purchase capital goods. Capital goods are the equipment, machinery, and products that companies purchase to expand operations and infrastructure are part of longer-term investment objectives. It becomes clearer, from this perspective, that the initial goals are to shift the cost differentials between both US and Chinese suppliers for common heavy equipment, with an eye to shift the balance of favor to US-based heavy equipment suppliers without having short-term impacts on consumer pricing. There will be a few odd crossovers in the initial July 6th list — for example, the Nest Thermostat from Google would be classified under 9032.10.00 Automatic thermostats.

Overview of Tariffs on Electronics Components

Our interest, however, lies in the items which are going to impact the electronics industry. Overall, we’re not heavily concerned about the tariffs on pick-and-place machines, soldering irons, inspection equipment, etc. There are two reasons for this: one, is that capital investments in equipment for businesses like ours are made based on multi-year plans; and, secondarily, our highest-ticket capital expenditures are typically sourced from the EU and US, based on the brands of equipment we buy which we feel are best suited to our production loads here in the US.

The tariffs that will impact us, and our customers, really begin around section 8532. These tariffs cover a wide range of products used in printed circuit board assemblies, including:

- Capacitors (all, including tantalum, aluminum electrolytic, and ceramic)

- Resistors (all, including thin/thick film, radial, potentiometers, and rheostats)

- Fuses

- Relays

- Switches (all, of any kind)

- Connectors and terminals of any kind for making electrical connections

- Transistors

- Thyristors

- LEDs

Any printed circuit assembly (8543.90.68 and 9030.90.68 serve as a catch-all) The second set of tariffs that have been suggested, but are not yet rolling out on July the 6th include the following impacting items as well:

- Diodes

- Integrated circuits (all, including processors, controllers, memory, amplifiers, other)

- Low-voltage Insulated wiring

Impacts of Tariffs on Component Shortages

As we’ve discussed before, one of the largest factors currently impacting electronics production is a severe under-supply of passives, e.g. resistors and capacitors. In general, we tend to expect that any increase in cost will reduce demand, but we do not see higher prices resulting in any freeing up of these components. Here are a couple of key reasons why:

Passives are not a discretionary purchase.

Companies need to build their products to sell them and increasing the price of components will increase the costs of those products. Only if the end product costs were to substantially increase would that reduce demand. Years of haggling on passive component prices reduced their value so significantly that little new production capacity was brought to market. The net result of this is that passives are a minimal driver on overall product cost for many items, meaning these tariffs alone would have little impact on the final product price to reduce demand sufficiently to overcome the market shortage.

Most passive consumption does not happen in the US.

The vast majority of thepassive demand these days goes into portable electronics and electronics for automobiles. The bulk of portable electronics (cell phones, tablets, etc.) are produced in Asia, and as such these tariffs would have little impact on their prices. While there is substantial automotive electronics production in the US, overall production is well spread worldwide, with significant capacity in Mexico, Eastern Europe, Japan, Korea, and China.

The primary impact these tariffs will have on US electronics production will be to drive the cost of these components higher, while providing little relief in a tight supply market. For most designs, price increases on passives will contribute little to the overall Bill of Materials (BoM) increase, as these passives are a minor contributor to overall BoM costs for most designs. However, competition for supply in high volume production will get more expensive in the coming months and may result in some orders seeing a substantial BoM increase to ensure supply in the hundreds of thousands.

Overall Impact on Product Pricing

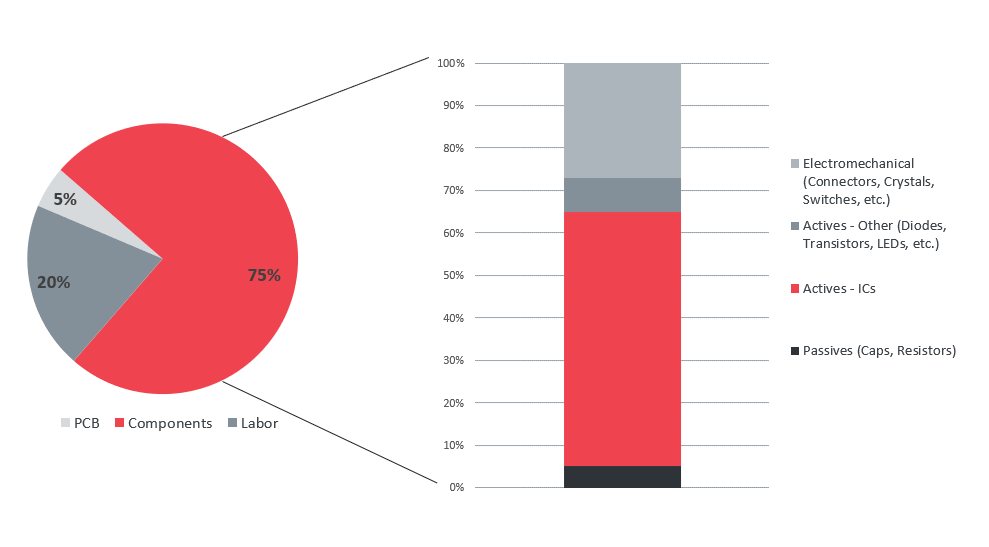

The first thing we can understand is that a 25% tariff on these items does not automatically equate a 25% increase in Cost of Goods Sold (COGS) for an electronics product. That is, making electronics in the US does not automatically get 25% more expensive. To understand this better, let’s take a look at the cost breakdown of a model US PCB assembly made in low-to-mid volumes (100’s to 1,000’s of units), representing a typical industrial product we might see:

Cost breakdown of a model US PCB assembly made in low-to-mid volumes (100’s to 1,000’s of units)

In this model, we can expect that all passives are impacted, half of our spend on actives – other, and about a quarter of our spend on electromechanical components. This results in a net impact of 3.9% increase to the Bill of Materials, or 2.95% increase on total Cost of Goods.

A 3% increase in COGS is certainly something we would concern ourselves with, but until we see tariffs hitting more of our actives, and especially integrated circuits, we’re still a long ways off from a 25% increase in total cost to produce electronics in the US.

Comparing the Impact of Tariff-Driven Prices Increases to Importing Work vs. Assembling in the US

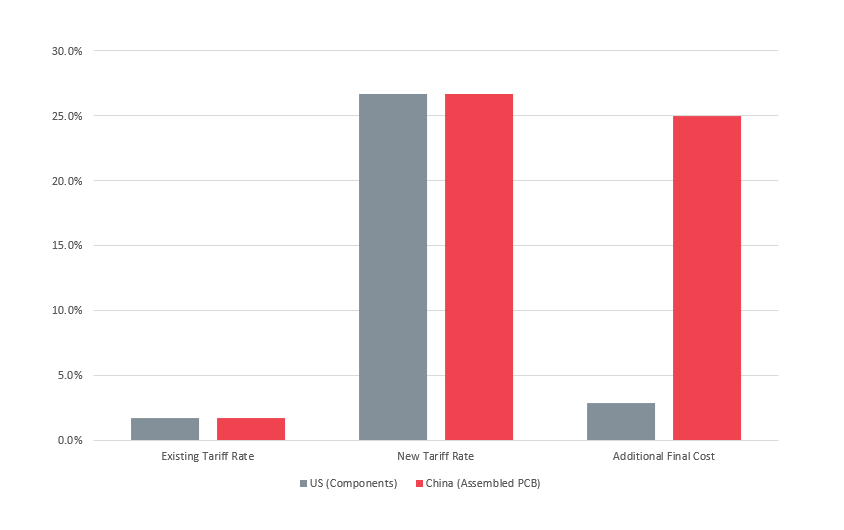

It’s worth noting that for many categories of electronics being imported as final goods to the US from China, the normal tariff rate is from 1.7-3%. But, let’s compare the cost of importing an assembled PCB from China to the US, vs. building that same device in the US under the new tariffs.

Let’s consider a product like the ESP-WROOM-32. If we’re to import it from China we’d pay an additional 25% in tariffs on top of the existing 1.7% in tariffs under section 8543. Therefore, current going price is $4.10, the price after the new tariffs would be $5.20. Based on our above analysis, if we could import the components to the US and build it here for less than a 25% premium over China prices, we’d save money by making it in the US.

The following graph details our breakdown on tariff impacts of assembling in the US vs. sourcing in China:

Impacts of Tariffs on The Future of US Electronics Manufacturing

Pricing increases on components have already started to impact prices on tightest supply components like capacitors and resistors, while other component price increases will work their way into the overall US market over several months as existing stock at distributors in their US warehouses is depleted. Component costs will largely stay fixed for a short period of time before rapidly raising.

If tariffs expand to integrated circuits, counterfeit materials will become a larger risk in the overall supply chain. Driven by high prices, the number of “too good to be true,” deals are going to increase and desperate purchasing managers and EMS buyers will be tempted to take the offer. Quality Contract Manufacturers (CMs) will continue to work only with authorized distributors as materials prices go up and availability goes down, as the risks for their customers will simply be too great.

We can expect further uncertainty from OEMs, startups, and small businesses with regards to international manufacturing. As trade issues continue to be front-and-center, we’ll see more low- to mid-volume electronics manufacturing either starting onshore in North America or moving back — even with elevated component prices, while large-volume electronics manufacturing remains overseas for the near-term.

Read about 2024 Trade Regulations affecting electronics and PCBA tariffs now.

With longer-term tariffs on existing materials, we’ll see more and more US-based electronics manufacturing purchasing shifting to Mexico to take advantage of low tariffs between China and Mexico, along with low final-product tariffs via NAFTA. Overall, we can expect the impact on tariffs on any goods to result in more multi-sourcing, making the same product in multiple global regions, as the risk of retaliatory tariffs increases and OEMs optimize for taxes. For US-based customers, CMs who offer both US- and Mexico-based production capabilities will see a marked increase in demand as customers seek to locate production to lower duty regions as US/China friction heats up.